Five years later, Russia still hasn’t recovered from its 2014 economic crisis. These graphs explain why.

Five years ago, Russians realized that their country was sinking into yet another economic crisis. On November 5, 2014, the Central Bank announced that it would no longer underwrite the value of the ruble. That fall, as Russian residents followed their currency’s downward slide with rapt attention, they still didn’t know that this crisis, unlike its predecessors in 1998 and 2008, would stretch on for many years. We’ve used infographics to show why even half a decade hasn’t been enough time for Russia to recover.

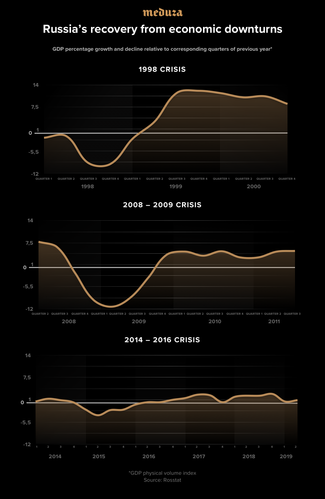

The crisis of the late 2010s wasn’t like its predecessors. After 1998 and 2008, Russia’s economy bounced back quickly. Not so today.

After the August 1998 downturn that capped Russia’s long, transitional post-Soviet period, the country’s economy began growing rapidly despite the ruble’s depreciation by almost five times and the government’s default on all its ruble-based debts.

At first, that growth was a sign of recovery: Manufacturing capacity that had remained idle since the Soviet era once again went into demand. Then, when the reforms of the 1990s and early 2000s were fully implemented, entrepreneurs began investing in new production facilities. As the Russian economy more broadly showed new signs of life, so did its market for oil: Over the course of the aughts, oil prices almost doubled.

That period of growth ended in late 2008, when a new recession swept in from the United States as the subprime mortgage bubble burst. The resulting crisis was the world’s worst since the Great Depression, and Western investors rushed to withdraw their funds from developing markets, including the Russian economy. As production rates in the U.S. and Europe fell, so did oil prices.

For several months, Russia’s Central Bank tried to keep supporting the ruble despite pressure from investors eager to buy up dollars instead. The bank finally caved in 2009, leaving the ruble to spiral into depreciation once again. Then, despite the government’s efforts to support big businesses, manufacturing went down, too: It soon became clear that many companies had borrowed dollars and euros, which their depreciating rubles could no longer pay back.

Nonetheless, that crisis didn’t last long: By the end of 2009, the Russian economy began to grow. When oil prices once again exceeded $100 per barrel, it seemed as though Russia would return to the growth rates it had seen in the 2000s. That never happened: The growth rates of the country’s GDP and its population’s income in the early 2010s were half of what they had been before the recession. The fact that the federal government had rolled back practically all of its earlier reforms by 2011 had a significant effect on that lack of recovery.

In 2014, oil prices fell once again. At the same time, Western countries began introducing sanctions to push back against the Russian government’s actions in Ukraine, which further deterred investors. Unlike the other crises, this one was not followed by a rapid recovery. Oil prices remained low, sanctions only became more severe, and investors from Russia and the rest of the world alike directed their funds elsewhere. By the end of 2016, the budget had been hollowed out, too, and those funding cuts represented yet another hit to manufacturing levels and quality of life in Russia.

In 2019, the country’s economic growth has remained weak: It is lower than the average national growth rate worldwide and even comes in below the growth rate in most developed countries.

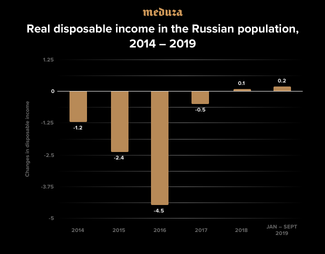

Russians aren’t seeing more income.

When adjusted for inflation, the average amount of money Russians make (including both salaries and other kinds of income) is actually less than it was in 2014. Average incomes rose very slightly for the first time since the crisis in 2018, and even that was only after Russia’s state statistics agency began using a new formula to calculate that figure. Meanwhile, the 2008 crisis only caused incomes to decrease for half a year, and following the 1998 crisis, average incomes soon began growing in earnest.

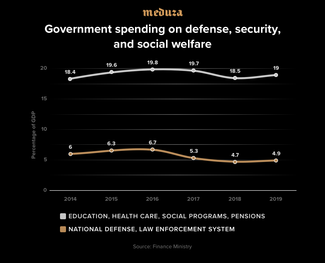

The Russian government hasn’t even been able to return defense spending to pre-recession levels.

In 2017, it became clear that the reserve funds Russia had accumulated in the preceding years while oil prices were high would soon be exhausted. All remaining reserves were transferred to the National Wealth Fund, and policymakers decided to leave that fund intact rather than using it to close the country’s budget deficit. That meant even more significant cuts in government spending, and the first programs to go were often in the very same areas that brought government leaders the most pride. For example, defense spending expanded rapidly in 2011 (leading Finance Minister Alexey Kudrin, who disapproved of that spending pattern, to resign), but that spending had been cut by more than 1.5 times by 2018. Because the military sector of Russia’s budget is confidential, it is impossible to say which specific programs were on the chopping block, but it is public knowledge that Russia postponed its mass purchasing program for the latest tank and airplane models.

Spending on social welfare, including health care programs, education, and pensions, saw less severe cuts. However, even now, as oil prices have recovered and Russia’s budget is once again in the black, the government has not restored its social spending to pre-crisis levels. Now, Russian policymakers have new priorities, namely a set of “national projects” that would focus on transportation and other infrastructure. Those projects were designed in the hope that they would finally enable renewed economic growth overall.

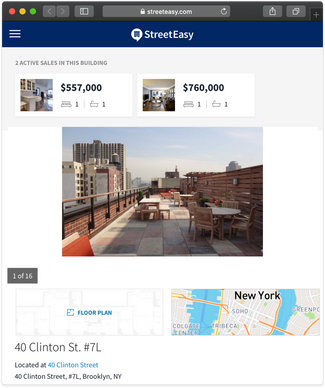

Real estate prices fell and never recovered. Just compare the New York apartments you could get in 2014 and today by selling your suburban Moscow crib.

Muscovites probably had no idea how rich they were in 2014. Despite their lower incomes, apartment owners in Russia’s capital were on the same level as their Western counterparts in terms of wealth.

Prices in rubles for Moscow real estate reached an all-time high at the end of 2014, and the ruble’s unusually high price at the time made Moscow apartments some of the most valuable in the world. Even selling a two-bedroom apartment in a residential district (like this $500,000 home in the Chertanovo area) in 2014 could get you a comparably large apartment in one of New York’s most fashionable neighborhoods, Brooklyn Heights. You could even get a view of the Manhattan skyline in the bargain. For buyers who would prefer more space, there were houses like this similarly priced McMansion with an expansive patio just a short distance from the shore on the edge of the city.

Five years later, however, the prices for Moscow real estate in rubles have fallen, the ruble itself has depreciated, and that very same two-bedroom in Chertanovo is fully half the price it used to be in dollars. New York prices have only risen in that same period, lowering the Chertanovo flat’s purchasing power to the level of a small downtown Manhattan studio.

Of course, central Moscow is still a very expensive place to live. If you’re selling an apartment on the Russian capital’s outskirts, you could only count on finding a comparably large apartment in New York far from downtown (at the northern end of the Bronx, for example).

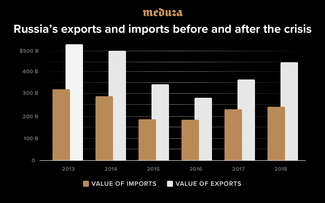

The Russian government did nothing to fundamentally change the country’s economy or phase out imports.

After oil prices dropped suddenly in 2014, Russian exports immediately fell, followed by the total value of the country’s imports

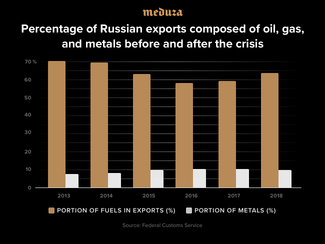

Low oil prices persisted for an extended period of time, a state that theoretically could have triggered a fundamental restructuring of the Russian economy. For example, the production of other goods suitable for export could have increased. However, none of that actually happened: The share of environmentally devastating fossil fuels and other raw materials in Russian exports remained essentially unchanged.

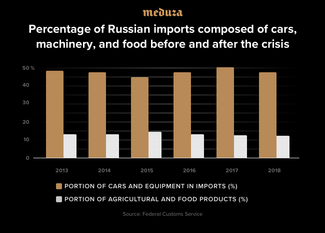

Hopes for a successful import phase-out in Russia also fizzled; only the domestic agriculture industry saw notable economic success. That growth was due in part to devaluation and in part to decreased imports from Europe, but its most important cause was the wave of investment in the industry that persisted throughout the 2010s. Regardless of the state of Russian agriculture, however, the country’s population as a whole paid the price for its inability to phase out imports. As Russian manufacturers began seeing less competition from abroad, Russian residents were forced to buy lower-quality goods for higher prices.

One sign of economic recovery is rising investment in manufacturing, especially when that investment takes the form of equipment purchases. In Russia, no such rise in purchases has been observed. Domestic production of industrial infrastructure has also fallen in the course of the past two years.

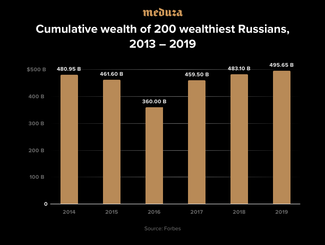

Only the richest Russians have recovered from the crisis.

Judging by Forbes’s ratings of Russia’s 200 wealthiest people, multimillionaires and multibillionaires did take a hit during the 2014 – 2015 economic crisis. By 2016, their combined wealth had fallen by almost $120 billion dollars (granted, that brought them to a total of $360 billion). In 2014, wealthy Russians had to have a net worth of $450 million dollars to make the top 200 list; in 2016, the cutoff was $350 million.

However, the finances of Russia’s richest quickly recovered. As early as 2018, they surpassed the total wealth record they themselves had set in 2013, before the crisis hit. In 2019, according to Forbes’s ratings, the total wealth possessed by Russia’s top 200 was $15 billion higher than it had been in 2014. Leonid Mikhelson, the oil magnate and Novatek chairman who leads the entire list, added $9 billion to his net worth in that time period, and anyone with less than $450 million to their name fell off the list once again.

Analysis by Dmitry Kuznets

Translation by Hilah Kohen