Unsavory sanitization How Russian banking regulators got rich on federal bailouts. A joint investigation by Meduza, Proekt, and VTimes.

In the spring of 2019, police in Russia arrested Colonel Kirill Cherkalin, the head of the Federal Security Service Banking Bureau’s Economic Security Department. In his home and his colleagues’ homes, officials found a record 12 billion rubles ($157.8 million). Immediately after these raids, Valery Miroshnikov — the first deputy director of the Deposit Insurance Agency (DIA), which flooded Russia’s banks with money in the mid-2010s — fled the country. While at the DIA, Miroshnikov worked closely with Cherkalin. Miroshnikov remains abroad today, but his name still echoes in Russia, where he features prominently in felony case evidence. Together with the news outlets Proekt and VTimes, Meduza explains how a deputy director at the Deposit Insurance Agency managed to collect tens of billions of rubles from bankers, and we explore who else got rich on the massive bankruptcies and bank restructurings (“sanitizations”) that are considered one of Russian Central Bank Chairwoman Elvira Nabiullina’s major achievements.

- In recent years, Russia’s Central Bank printed an enormous sum of money in a campaign to restructure the country’s major banks and liquidate smaller failing financial institutions. Meduza and its media partners spoke to sources and obtained testimony from witnesses who described vast abuses of authority by senior officials in the Deposit Insurance Agency (DIA), a Russian state corporation responsible for various insolvency procedures.

- Case evidence suggests that former DIA First Deputy Director Valery Miroshnikov helped “Alfa-Bank” restructure “Balt Bank” in exchange for millions of dollars in kickbacks, which he allegedly shared with banking officials in Russia’s Federal Security Service.

- DIA Director Yuri Isayev allegedly facilitated Arkady Rotenberg’s takeover of “Mosoblbank,” just as the oligarch was hit by U.S. sanctions and desperately needed the Russian state’s assistance.

- After several years in office, Russian Central Bank head Elvira Nabiullina ultimately stripped the DIA of its role in bank restructurings. It apparently took as long as it did because of Yuri Isayev’s close ties to Russia’s police and national security establishment.

Kirill Cherkalin has spent more than a year and a half in pretrial detention. Now bearded and long-haired, he’s plea-bargained with prosecutors and testified against his former colleagues, implicating Dmitry Frolov (his department’s ex-deputy director) and detective Andrey Vasilyev in a bribery scheme that amassed wild sums of money. A source with knowledge of the investigation told Meduza that Russian bankers have lined up to describe how they were essentially robbed by these men.

According to Cherkalin, however, most of the cash found at his home actually belonged to Valery Miroshnikov, the former deputy director of Russia’s Deposit Insurance Agency. When Cherkalin was arrested, Miroshnikov either left Russia immediately afterward or was already abroad in Australia. Either way, he never returned home. Two and a half months later, the DIA announced Miroshnikov’s resignation without explaining why he was stepping down.

No one directly involved in the case agreed to speak on the record to Meduza, but Alexander Zheleznyak (who served as Probusinessbank’s board chairman until the Central Bank revoked its license) says Miroshnikov was, in fact, the brains behind the corruption scheme.

A banking sector purge

Vladimir Putin endorsed Elvira Nabiullina to lead Russia’s Central Bank in 2013 after she spent a year as his presidential adviser and four years as economic development minister. Several major bankers told Meduza that Putin granted her carte blanche to take decisive action in her new role, and that is precisely what she did, revoking the licenses of bad-actor banks that the Central Bank had tolerated for years.

In the past seven years, under Nabiullina’s leadership, the Central Bank has revoked nearly 500 banking licenses and bailed out roughly 30 banks (financially restructuring institutions that collected too many bad debts). In that time, several of Russia’s biggest bankers and financiers fled the country after encountering sudden business problems. Almost all of them have now been charged with embezzling billions of rubles.

The Central Bank’s new zero-tolerance policy and radical measures against corruption meant a far more powerful role for Russia’s Deposit Insurance Agency, which has managed enormous assets and funneled 1.5 trillion rubles ($19.7 billion) in public money since 2013.

The money maverick

Multiple sources in Russia’s financial sector who spoke to Meduza for this story described Valery Miroshnikov as a talented, experienced manager who knows how to navigate the industry and make money. One banker even called him a “genius.”

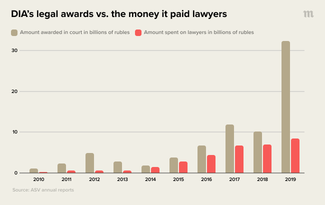

According to two sources, Miroshnikov owed most of his “earnings” to banks going bust after they lost their licenses. In normal bankruptcies, creditors themselves can appoint an insolvency administrator, but Russian law says only the Deposit Insurance Agency can manage bankrupt banks. In other words, the DIA seizes control and “changes everything,” hiring from its own small pool of accredited firms to handle security, legal representation, and accounting. The process is not enormously competitive. In fact, in September 2020, Russia’s Federal Antimonopoly Service criticized the lack of transparency in the DIA’s hiring practices.

Miroshnikov was responsible for choosing the lawyers needed to sue for outstanding debts. The attorneys he hired were paid handsomely, earning millions of rubles in fees and collecting percentages of assets recovered to bankruptcy estates. In some cases, like with “Probusinessbank,” the attorneys even claimed percentages from loans that were repaid voluntarily without any legal action needed.

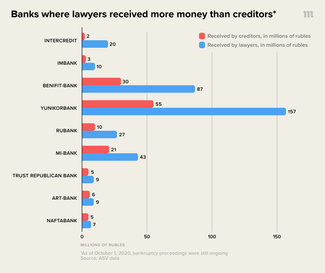

The Deposit Insurance Agency has also raised concerns by selling off bankrupt banks’ property at low prices. In November 2016, for example, the agency sold “Poidem!” bank (acquired from Probusinessbank) in closed bidding for 380 million rubles ($5 million) — less than half the asking price. To complicate matters further, the buyer “Sovcombank” soon resold Poidem! to top managers at “Russian Capital,” a DIA subsidiary bank.

This was quite the bargain; just before Probusinessbank lost its license, it nearly sold Poidem! to “VTB Group” for 3 billion rubles ($39.2 million), a source told Vedomosti. Over the next two years, moreover, the Poidem’s new owners collected almost 2 billion rubles ($26.2 million) in dividends. Probusinessbank contested the sale, arguing that its asset was undervalued, and it lost three lawsuits before Russia’s Supreme Court overturned the previous verdicts and ruled in February 2019 that the DIA may have acted in its own interests.

According to the agency’s annual reports, the DIA recovered 32.4 billion rubles ($424.1 million) from debtors through lawsuits in 2019 on a legal budget of 8.5 billion rubles ($111.3 million), 39 percent of which was spent on bankruptcy management. Over the course of the year, creditors of bankrupt banks got back about 45 percent of their money — a reasonable figure, says “Pepeliaev Group” partner Yulia Litovtseva, but that money came mostly from debts secured by collateral.

In all these dealings and transactions, the businesses that kept funds in bankrupt banks were the real losers. These firms were always last in line to get their money back.

How to lose your life savings

In February 2016, Russia’s Central Bank erased most of Dmitry Protasyev’s life savings when it revoked Interkommerts’s license, wiping out the 20 million rubles ($261,600) the ship mechanic had set aside for retirement. Protasyev’s story is not unique.

After seizing control of Interkommerts, the DIA paid out 64 billion rubles ($837.1 million) to depositors. Though this was a record amount at the time, the bank still owed another 3 billion rubles ($39.3 million) to people like Dmitry Protasyev, whose savings exceeded the 1.4 million rubles ($18,325) insured by Russia’s federal government. Businesses lost another 18 billion rubles ($235.6 million) in current accounts and other funds held at Interkommerts.

By Russian law, a bank that loses its license is declared bankrupt and placed in receivership, which the Deposit Insurance Agency manages. The DIA is responsible for selling off the bank’s assets, collecting outstanding debts, and bringing charges against any administrators who committed wrongdoing. The agency deposits this money into an insolvency estate and then distributes the funds to the bank’s creditors (including the DIA itself, now that it’s covered the bank’s deposit insurance payments).

In the case of Interkommerts, the Deposit Insurance Agency pressed charges against three of the bank’s former senior executives and its former board chairman, Alexander Bugavevsky. No other shareholders have been held responsible for the bank’s collapse. Spokespeople for the DIA say the agency still has no “legal basis” to go after anyone else, but the selective response has irritated some. Multiple sources told Meduza that the DIA’s legal methods are often frustratingly opaque.

In the five years since Interkommerts went bust, the Deposit Insurance Agency has recovered just 8.5 billion rubles ($111.3 million) — including almost 2 billion rubles ($26.2 million) collected through lawsuits — for the bank’s insolvency estate. The process has stalled; in four years, the statute of limitations will expire and make it impossible to hold other senior executives, shareholders, and beneficiaries responsible.

Except in specific exceptions, the Central Bank is prohibited from meddling in the DIA’s bankruptcy-management operations.

Too big to fail

Dmitry Protasyev and others could have kept their savings if Russia’s Central Bank had elected to restructure Interkommerts instead of liquidating it. Bailouts are expensive, however, and officials go this route only when they decide that an institution’s bankruptcy would be too socio-economically damaging.

Banks continue operating while they’re being restructured and only the owners lose money. The Central Bank chooses larger institutions to act as insolvency managers, loaning them the money needed to plug excess liabilities at a 10-year fixed interest rate of 0.51 percent. While being restructured, banks are exempt from standard regulations — an important loophole that allows insolvency managers to dump their bad assets into these institutions.

Until recently, the Deposit Insurance Agency was responsible for calculating the Central Bank’s options with specific banks and deciding whether a bailout or liquidation was necessary, a major banker told Meduza. The same source says the DIA also determined how much money was allocated to restructure the institutions that got bailouts.

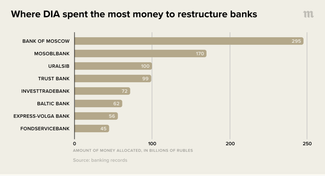

Russia’s Central Bank has printed 2 trillion rubles ($26.3 billion) to restructure various banks through the DIA; two-thirds of this money was allocated in the past seven years. Moscow Exchange Supervisory Board Chairman Oleg Vyugin, who used to work at Russia’s Central Bank, explained to Meduza that the cost of bailouts often spirals because insolvency management shakes an institution’s foundations, chasing away business and expanding the shortfall that imperiled the bank in the first place.

After August 2014, in coordination with the Central Bank, the Deposit Insurance Agency started selecting insolvency managers for restructured banks by soliciting competitive bids. The eligible applicant that quoted the smallest price was supposed to get the job, which is itself fraught with risk, given the lack of due diligence that’s possible in the short turnaround required. However, because restructured banks are exempt from standard regulations, there are actually powerful incentives for institutions with their own problems to get involved and offload their junk assets.

This situation encouraged bad behavior that was made worse by the DIA’s own corruption. According to Vedomosti, the bidding process used to select insolvency managers was riddled with graft; the real competition wasn’t over restructuring services but who could pay the biggest bribes (which reportedly ranged from 3 to 5 percent of the entire amount allocated in a bailout). One banker who fled Russia told Meduza that kickbacks went not just to the Deposit Insurance Agency but also to the Central Bank itself, as well as banking officials in the Interior Ministry and Federal Security Service.

The “action plan” in Miroshnikov’s safe

Nearly every source who spoke to Meduza confirmed that any bank bailout couldn’t move forward without involving Valery Miroshnikov. Meduza also obtained testimony from the Cherkalin case describing how Miroshnikov intervened in a dispute in 2014 between Oleg Shigaev and Andrey Isayev, the co-owners of “Balt Bank.” Isayev says Shigaev tried to swindle him by voluntarily surrendering their bank to the DIA and “Alfa-Bank” for restructuring in exchange for an unofficial payoff, leaving Isayev with nothing.

According to witness testimony, Oleg Shigaev did, in fact, seek out the Deposit Insurance Agency, but soon got in over his head. After falling out with his partner, he hired a lawyer named Vakhi Gishkaev who later arranged a meeting with Miroshnikov. The group met at a restaurant, joined by Alfa-Bank Board Chairman Andrey Sokolov, who expressed Alfa-Bank’s readiness to act as Balt Bank’s insolvency manager. At a second meeting (this time at a cafe, according to Gishkaev’s testimony), Sokolov and Miroshnikov asked to see Balt Bank’s books. Shigaev agreed.

The process started slipping away from Shigaev by the third meeting (held in a private dining room at another restaurant without Miroshnikov), when Sokolov revealed that an “express analysis” of Balt Bank’s accounts uncovered 30–33 billion rubles (about $413.3 million) in excess bank liabilities. When Gishkaev protested, saying this was impossible, Sokolov allegedly explained that the figure was inflated to get a subsidized loan from the Central Bank for 60 billion rubles ($792 million).

According to Gishkaev, Sokolov exaggerated the numbers so Alfa-Bank could earn at least 10 billion rubles ($132 million) on the bailout. Miroshnikov allegedly collected an additional 1 billion rubles ($13.2 million) in kickbacks, which he supposedly distributed among officials in the FSB’s Banking Bureau. Asked about Gishkaev’s testimony, a source at Alfa-Bank told Meduza that the lawyer is merely angry about being left out of the deal; Gishkaev allegedly offered to sell out his client for a piece of the bailout.

Based on Gishkaev’s testimony, Balt Bank’s fate was decided in a final meeting at Miroshnikov’s office in August 2014, when the DIA official allegedly threatened a reluctant, stunned Oleg Shigaev with criminal prosecution and the outright liquidation of his business, if he refused to submit voluntarily to Balt Bank’s restructuring. Gishkaev says he encouraged his client to ask for a payout of a few billion rubles — at least 2 billion rubles ($26.4 million) — to recover the capital Shigaev had personally invested in Balt Bank. Miroshnikov then allegedly told Shigaev and Sokolov to draw up an informal, confidential “action plan” ensuring that Sokolov would pay this money to Shigaev “in the form of gratitude.” Miroshnikov vowed to guarantee the payment and supposedly stashed the plan in his safe, before contacting the Central Bank to initiate the voluntary restructuring.

On August 20, 2014, Russia’s Central Bank approved Balt Bank’s restructuring and allocated 57.4 billion rubles ($757.7 million) for a bailout. Alfa-Bank was soon tapped as the insolvency manager.

Russia’s Deposit Insurance Agency declined to comment on Gishkaev’s allegations. Spokespeople for Alfa-Bank told Meduza that none of its employees has been investigated for any wrongdoing in Balt Bank’s restructuring, and Andrey Sokolov says Vakhi Gishkaev’s claims about bribes and “action plans” are untrue.

Andrey Isayev challenged the restructuring, losing three lawsuits against Alfa-Bank, including a Supreme Court hearing. Today, both Isayev and Shigaev are wanted in Russia for fraud.

170 billion for Rotenberg

At the Deposit Insurance Agency, Valery Miroshnikov reported to Yuri Isayev, who Meduza’s sources say usually avoided direct involvement in bank restructurings and preferred instead to handle the DIA’s strategic affairs, coordinating with the Finance Ministry and the Central Bank. He apparently broke that pattern, however, when the influential billionaire Arkady Rotenberg decided to gobble up “Mosoblbank,” which was owned at the time by Andzhey Malchevsky and his son Alexander.

In late 2013, amid tensions between Mosoblbank’s owners and Russia’s Central Bank, the Malchevskys were approached by two heavy-hitters who wanted a piece of their business: “Ritual-Service” co-owner Oleg Shelyagov and Judo Veterans’ National Union head Pavel Balsky, who also served on the board of directors of SMP Bank, which belongs to Arkady Rotenberg. Alexander Malchevsky later told a fellow banking executive that Shelyagov and Balsky had claimed to represent Rotenberg; Balsky even allegedly summoned Yuri Isayev to their first meeting and said he would “supervise things from the DIA.”

Alexander Malchevsky’s lawyer declined to comment on these allegations, and Yuri Isayev told Meduza that he recalls no such meeting.

In exchange for a stake in Mosoblbank and a chunk of the Malchevskys’ other businesses, Shelyagov and Balsky supposedly promised to make the family’s regulatory problems go away. “We know you have ‘hemorrhoids’ with the Central Bank,” they allegedly said.

A source told Meduza that the Malchevskys even donated 120 million rubles ($1.6 million) to the “Dynamo” Moscow hockey team (which Isayev managed for three years) and another 30 million rubles ($394,690) to the Judo Veterans’ Union as a “demonstration of their readiness and willingness to work with the Rotenbergs.”

At first, Shelyagov and Balsky allegedly sought a 25-percent stake in Mosoblbank. This later grew to 50 percent and then ballooned to 75 percent.

Oleg Shelyagov told Meduza that these negotiations never took place. He says his dealings with Mosoblbank’s previous owners were always about restructuring the bank, which he insists was in bad financial shape. Shelyagov also says he became involved in the bailout process as an adviser at Valery Miroshnikov’s request. Shelyagov wasn’t authorized to represent Arkady Rotenberg, he says.

Representatives for Arkady Rotenberg declined to comment for this story. Pavel Balsky did not respond to Meduza’s questions. Spokespeople for the Deposit Insurance Agency also declined to comment.

Whoever was representing whom, Mosoblbank was ultimately restructured, not resold, and Rotenberg’s SMP Bank was selected as insolvency manager. Shelyagov became Mosoblbank’s new director and Balsky joined the board of directors.

Mosoblbank’s bailout was especially fortuitous for Arkady Rotenberg, whose SMP Bank started hemorrhaging money in April 2014, after U.S. sanctions targeted the institution in response to Russia’s annexation of Crimea. In just two days, the bank lost more than 10 billion rubles ($131.7 million). A month later, the Central Bank decided to restructure Mosoblbank for more than 170 billion rubles ($2.2 billion) — the second-most costly restructuring of a single bank in Russia’s history. Without soliciting competitive bids, the Central Bank selected SMP Bank to act as insolvency manager.

Andzhey Malchevsky was subsequently indicted for illegally withdrawing money from Mosoblbank’s depositors and investing the cash in real estate and other assets, replenishing old accounts with money from new clients in what amounted to a pyramid scheme. He pleaded guilty, “took steps to repay the damages,” and later died in prison from meningitis. His son fled the country before being arrested in absentia for felony fraud.

In 2015, Mosoblbank served as the processing center for Rotenberg’s grand construction of the Crimean Bridge, which won the billionaire a medal from President Putin. Despite this big business, Mosoblbank has closed most of its 600 branches across Russia. The bank has been running a deficit for more than five years now; as of October 1, 2020, its accounts stood at negative 133 billion rubles ($1.8 billion). Spokespeople for SMP Bank told Meduza that the restructuring is proceeding according to plan and will be completed in 2031.

These pipes are clean

A government official in Russia’s financial-economic wing told Meduza that Elvira Nabiullina always harbored suspicions about the Deposit Insurance Agency’s role in bank restructurings. She had to wait a couple of years before pressing the issue, however, due to Yuri Isayev’s powerful backers in Russia’s police and national defense infrastructure.

In 2015, Nabiullina finally started discussing the DIA’s ineffectiveness openly, and the Central Bank also began drafting legislation to entrust bank bailouts to a new agency called the Banking Sector Consolidation Fund (FKBS). The Deposit Insurance Agency was suddenly vulnerable and Nabiullina’s criticisms were well-timed; then Deputy Prime Minister Igor Shuvalov supported her initiative, and others started raising concerns about Valery Miroshnikov, with some officials even taking their worries directly to Alexander Bortnikov, the head of Russia’s Federal Security Service. In 2017, the new legislation took effect, removing the DIA from future bank restructurings.

In late October 2020, Nabiullina announced that the Central Bank’s rehabilitation efforts in Russia’s banking sector were finally complete. All in all, the campaign cost roughly 7 trillion rubles ($90.1 billion) — 3.8 trillion rubles ($50 billion) of which the Central Bank poured into bailouts through FKBS, including the restructuring of major institutions like “Otkritie,” “B&N Bank,” and “Promsvyazbank.” Insolvency managers and restructured banks themselves have already repaid or are still repaying some of this money.

The Deposit Insurance Agency has been booted from handling new bailouts, but it’s still managing the reorganizations it started before the Banking Sector Consolidation Fund took over. The DIA is still responsible for compensating depositors and liquidating banks, but the agency now faces new restrictions. Following the outcry about the exorbitant fees paid to outside lawyers, the DIA has started hiring in-house attorneys. Russia’s Federal Antimonopoly Service, moreover, is advocating legislation that would force the DIA to adopt more transparent accreditation procedures for its contractors.

Despite the serious corruption allegations against his former subordinate, Yuri Isayev has emerged unscathed. In August 2020, President Putin even pinned a medal on him. A very different welcome awaits Valery Miroshnikov, should he ever set foot again in Russia. A source in the federal government told Meduza that Miroshnikov was written off as a criminal, the moment he fled the country.

Story by Anastasia Yakoreva (Meduza) and Boris Safronov (VTimes) with additional reporting by Roman Badanin (Proekt) and editing by Tatiana Lysova

Abridged translation by Kevin Rothrock