The evictors For the past five years, loan sharks have forced more than 500 Muscovites from their homes. Here’s how the industry works.

In Moscow and the surrounding region, there’s a whole industry of what are known as “black creditors” — microfinance institutions (MFOs) that deceive and seize debtors’ homes. Meduza managed to find almost 500 apartments lost by their owners over the past five years without so much as a court order. In fact, this scheme involves more than simply “squeezing” people from their homes, and it is possibly part of a wider, international money-laundering system. Meduza special correspondent Ivan Golunov explains the ins and outs of this industry.

The nuts and bolts of this report, broken down into five points

What Meduza discovered:

- Microfinance (or microcredit) organizations (MFOs) are often used in schemes to cheat debtors out of their homes. Meduza found more than 500 such cases over the past several years in Moscow and the surrounding region.

- It works like this: the borrower signs a home equity loan, and microfinance companies use various tricks to fool clients into agreeing to disadvantageous or impossible repayment conditions. Sooner or later, the debtor violates the contract, at which point their home becomes the property of the MFO or someone affiliated with the company. Defrauded borrowers are often evicted from their homes using threats and even violence, and there are job postings online advertising “evictor” vacancies at microfinance companies.

- The average lifespan of an MFO is about 18 months, and these businesses are sold online for several hundred thousand rubles (a few thousand dollars) as ready-made turnkey companies. MFOs change names, but their addresses, staff, and other company data remains the same.

- MFOs actively recruit investors to obtain the money they use to issue loans. In several cases, MFOs have turned to investment from foreign citizens and banks that have been implicated in international money-laundering schemes.

- Experts say the existence of these home-equity-loan schemes is evidence that the industry is under-regulated, and Russia’s State Duma recently introduced draft legislation that could seriously complicate the work of these fraudsters.

In the summer of 2015, Natalia Smelnitskaya was diagnosed with cancer. Despite government assistance and her job at a Moscow consulting company, she needed additional money to pay for an operation. So she took out a personal loan at a three-year 36-percent annual interest rate from Sovkombank for 2.7 million rubles ($41,420), with monthly payments of 80,000 rubles ($1,225). The surgery was a success.

Natalia made her payments on time, but the high interest rate was a heavy burden. When a colleague encouraged her to refinance with a private lender, she did exactly that, reaching an agreement with a company called “Loan Center 365” to refinance her loan at a slightly more manageable 28 percent. The catch? As collateral, she had to put up her four-bedroom apartment off Yaroslavskoye Highway.

According to Natalia, the loan center staff staged a commotion when it came time to sign her refinancing agreement. She says they hurried her when she tried to read the paperwork, and at one point the manager pulled a sheet from the stack of documents and said there’d been an error. Then she reprinted the page and asked Natalia to sign it again. For the next six months, Natalia paid regular 80,000-ruble installments. One month, however, her salary arrived late, and she was a few days overdue with her payment.

On the evening of December 26, 2016, Natalia received an unexpected visit from Anton Titov, an employee at Loan Center 365, who came to inform her that the company now owned her apartment, because of the late payment. Titov quickly reassured her, however, that she could remain in the home while repaying her loan. To keep a roof over her head, all Natalia needed to do was sign a renter’s agreement with Loan Center 365, requiring her to transfer 35,000 rubles ($535) every month to someone named Natalia Kovaleva (who, it later turned out, works at a firm called “United City Real Estate Service”). Natalia tried to call Loan Center 365, but nobody answered the phones. After finding out about Smelnitskaya’s problems, her employer even tried to repay her loan for her, but the money bounced back from Loan Center 365’s bank account.

As soon as February 2017, Loan Center 365 sold Smelnitskaya’s apartment, and in August that year she lost a lawsuit challenging her family’s eviction. Natalia’s ex-husband and two daughters, ages 13 and 22, were also registered in the apartment, but child protective services did not object to their eviction.

In December 2018, marshals came to Smelnitskaya’s home to evict her family. During this entire process, Natalia says, the new owner’s interests were represented by his mother, while the new owner himself remained in pretrial detention on charges of illegal drug possession. (Meduza’s source in law enforcement confirms this information.) After the family was removed from the apartment, the home was sealed off, with all their belongings still inside. A few days later, when Natalia stopped by to visit her old neighbors, she noticed that the seal on the door was broken, and there were sounds coming from inside the apartment, as if someone was smashing the furniture. Responding police officers arrested several men who claimed that they were helping to haul away what was left inside the home.

Today, Smelnitskaya’s apartment is sealed off, once again, and the local police precinct has opened a preliminary fraud inquiry into the operations of Loan Center 365. In Mytishchi, meanwhile, the company already faces felony fraud charges, though the investigation so far hasn’t led to any results, and the regional prosecutor’s office has tried repeatedly to close the case.

How “shady” credit schemes work

Loan Center 365 isn’t the only business using these methods to force people from their homes. Meduza managed to find several dozen analogous firms. As a rule, these companies don’t operate for longer than 18 months, before re-registering as new legal entities. According to Meduza’s calculations, these enterprises have managed to evict at least 500 families throughout Moscow and the surrounding region.

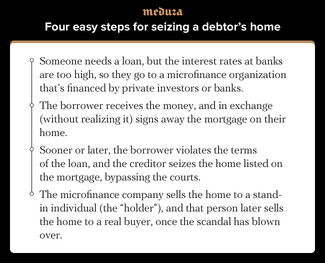

The families’ stories are virtually identical. When signing the home equity loan, the client signs over their apartment as collateral or reaches an apartment sale-and-purchase agreement. Borrowers are told that it’s something like a mortgage (sometimes they call it a lease), when the apartment is held as collateral by the bank until the loan is repaid in full. In a bank mortgage, however, the property can only be seized by court order, following overdue payments and visits by collectors, at which point the home is then auctioned off to the highest bidder. When obtaining loans from microfinance companies, victims sign over power of attorney and agree to other conditions that can be used to seize their property without a court order, transferring their apartment to an intermediary, and leaving the client with nothing.

The victims of predatory lenders rarely manage to get their homes back. For example, one debtor produced a schizophrenia diagnosis, which led a judge to nullify his microfinance agreement. In another case where the court sided with a debtor, the verdict describes a story that applies almost perfectly to hundreds of other victims: “A large number of documents were signed at the [Loan Center 365] office, so that [the debtor] could sign, without reading, a settlement agreement [for his apartment] as part of a number of previously agreed documents. However, the plaintiff did not intend to transfer the apartment to the defendant, which is also indicated by the lack of consent from his spouse,” ruled the Dorogomilovsky District Court, which invalidated the debtor’s settlement agreement with Loan Center 365. The court likely sided with the plaintiff because of his high social status. (A source familiar with the case told Meduza that the lawsuit was brought by a veteran of Russia’s intelligence community.)

Even clients who never fall behind on their loan repayments can still lose their homes. When Svetlana Podelskaya’s beloved summer cottage burned down, her children promised to help shoulder the rebuilding costs. But she decided to handle it on her own, and turned to the International Credit Bureau (MKB) in Moscow’s Brateyevo District for a 600,000-ruble ($9,190) loan, secured on her apartment. She found the company through an online ad. She made all her monthly loan repayments, and after 18 months she got a call from MKB’s manager, who informed her that she was receiving a two-month “credit holiday,” as a reward for being a “good debtor.” So Podelskaya skipped her next two payments, and before long a man showed up at her doorstep, introducing himself as the apartment’s new owner. When she confronted MKB, the manager denied having called her, and she had no paperwork to document the “credit holiday” offer. According to her loan agreement, Podelskaya forfeited her apartment, if she fell behind at least two months in her repayments.

Several other MKB clients have reported similar incidents over the years.

Podelskaya’s apartment was sold to an unemployed man named Denis Baluev. In court, Baluev was asked to reveal the source of the money he used to buy the home. After resisting the request, he finally produced a supplemental agreement to a loan contract with the microfinance company “Capital Loans” (Meduza obtained a copy of this document). The agreement doesn’t specify the loan amount, which was issued at an unusually low rate of 14 percent. The company Capital Loans shares a business address with MKB, and it’s managed by a Latvian national named Ivan Dubin, who also works at the International Credit Bureau. All three founders of Capital Loans are also Latvian nationals. There are several more companies also registered at MKB’s address, also owned by Latvian nationals who also work at MKB, and each serves a particular purpose. For example, “Mosarenda” LLC is typically used to confiscate debtors’ property rights.

Podelskaya is still litigating her case. At one of her hearings in Nagatinsky District Court, a man named Alexander Loginov came to represent Denis Baluev. Loginov is well known to debtors in Moscow, having managed the forceful eviction of many people who borrowed money from MKB and Loan Center 365. In December 2018, Loginov was convicted of multiple felony charges, including forcible assertion of private right and mild-to-moderate willful damage, and sentenced to 18 months in prison. His daughter, Galina Kieva, previously worked for Russia’s Federal Agency for State Registration (Rosreestr), where she handled the processing of real estate contracts. Since the early 2010s, she’s served as chairperson of the privately owned Economic Disputes Arbitration Court. In the first years that MKB operated, this commercial arbitration court was named in MKB contracts as the place to resolve disputes with debtors.

Of all the predatory companies in Moscow offering home equity loans, the International Credit Bureau has the highest number of victims, according to Meduza’s investigation. Former clients identified 99 instances where the company’s debtors lost their homes, as well as some cases where former homeowners who took loans from MKB could not be located. The main clientele for these enterprises is older people who are neglected by their families, in addition to other vulnerable groups. Even in better circumstances, credit managers try to drive a wedge between potential clients and their relatives. Svetlana Podelskaya recalls how managers at MKB advised her not to tell her children about her loan, arguing that young people are biased against loans, and the amount was relatively small, anyway. Her sons only learned that their mother had turned to a microfinance organization when the neighbors called them to say that representatives of the home’s new owner were cutting off the front door to the apartment.

Often, relatives can’t find out independently that an apartment has been signed over as collateral, because microfinance organizations don’t register these contracts with Rosreestr. The actor Sergey Frolov, whose story made headlines in March 2019, learned about his mother’s home equity loan several years after her death, when he discovered that the apartment he’d inherited from her had been sold at auction. Before she died, Frolov’s mother borrowed 600,000 rubles ($9,215) at a 28-percent interest rate from MKB, but her pension wasn’t enough to cover the monthly installments. Her loan paperwork, however, contained an income statement that significantly exceeded the amount of her retirement earnings. When the elderly woman couldn’t make her monthly payments, MKB convinced her to accept a 1.2-million-ruble ($18,445) loan, secured on her apartment. When she died, MKB seized her home to cover her unpaid debt.

What’s Latvia got to do with it?

Svetlana Podelskaya recognizes the smiling loan manager Sergey and remembers his Baltic accent from a photograph in the Latvian newspaper Dienas Bizness, in an interview with “AS West Kredit” Board Chairman Sergey Malikov, titled “Losing ABLV Bank, We Lose the Best.” In the article, Malikov criticizes the Latvian government’s policy toward banks that hold accounts for clients from former Soviet countries. “It’s geopolitics. These days, the Americans won’t let people from the former USSR — Russians, Belarusians, Ukrainians — feel comfortable with their own money. We need to understand that this action was not primarily directed against the shareholders of any bank, but against the customers [...],” he says. “What’s the model of these non-resident banks? They collect money from the former USSR because it’s quiet and calm here. This money is invested in securities, or loans are issued to the same non-residents who don’t want to borrow from some Scandinavian bank. [The Americans] want to eliminate this model.”

In February 2018, the U.S. Treasury Department’s Financial Crimes Enforcement Network (FinCEN) announced plans to impose sanctions against Latvia’s ABLV Bank, one of the three biggest credit institutions in the country, on charges of money laundering, aiding North Korea’s nuclear program, and illegal actions in Azerbaijan, Russia, and Ukraine. FinCEN also accused the bank’s executives of paying bribes to influence state officials in Latvia.

A week after the U.S. Treasury’s announcement, ABLV began liquidation procedures, while the Latvian authorities ordered the bank to reduce its share of non-resident clients. According to regulators, 36.7 percent of all banking operations in Latvia are performed by offshore companies. Among the transactions involving non-residents’ accounts, offshores are responsible for 44.5 percent. Latvian banks played an important part in schemes to move money out of Russia. In their “Laundromat” investigative report, journalists at Novaya Gazeta and OCCRP explained how these institutions were used to withdraw more than $18 billion from Russia over three years. The clients of these Latvian banks were mostly Russians who couldn’t open accounts at banks in Scandinavia and other more prestigious regions.

One of the banks hit hardest by the new restrictions on non-resident accounts was “Rietumu,” where assets plummeted 46.3 percent (1.4 billion euros, or $1.6 billion) in the first nine months. Latvia’s fifth largest bank, Rietumu was founded in 1992 by Leonid Esterkin and his brother-in-law, Arkady Sukharenko.

Sergey Malikov is the founder of the microfinance company “Mateks Credit” (later renamed “West Kredit”), which has issued home equity loans in Latvia since 1995. Malikov’s main credit investor was Rietumu bank, which opened a 20-million-lats (roughly $31.6-million) line of credit for the company in 2008, and then loaned Mateks Credit an additional 8 million euros ($9 million) in 2011, as well as another 24 million euros ($27 million) in 2016.

According to official records, Mateks Credit didn’t borrow only from banks. In 2009, the company received a loan of 1.1 million euros ($1.2 million) at a 10-percent interest rate from the British firm “Adovert Consult LLP,” based on West Kredit’s annual report in 2011. British records say Adovert Consult was created just a few months before the loan was issued, and it was liquidated soon after the loan was repaid. The LLP’s owners were listed as two Belize offshore companies: “Advance Developments Limited” and “Corporate Solutions Limited,” which feature in several investigative reports about a network of British enterprises that were used to launder $2.9 million from former Soviet countries.

Like in Russia, Mateks Credit’s work in Latvia also involved scandals surrounding the forceful eviction of debtors. In one case, Mateks hired a security company to “clean” a residence, and staff broke into a pregnant woman’s home and pepper sprayed her. In another incident, staff dismantled a home’s window and front door, in order to evict the residents. In the late 2000s, Mateks Credit’s reputation was in crisis, and consumer rights officials opened an investigation into the company. To make matters worse, Latvia also introduced tougher regulations on credit financing.

In 2011, Malikov and two other Latvian nationals created a new company in Russia: the International Credit Bureau (MKB) — the same firm that issues shady home equity loans to Muscovites. One of Malikov’s co-founders was Andis Anspoks, who a decade earlier served as secretary for an advocacy group in Riga called “For a Latvian Society Without Homosexuals.” In this group, Anspoks volunteered alongside Andris Baumanis, a lawyer whom the Latvian police suspect of paying bribes to judges.

The first Russian apartments seized by MKB were transferred to Malikov’s personal property, and according to Rosreestr he immediately signed them over to Rietumu bank as collateral for a $750,000 personal loan. In 2013, Rietumu opened a 20-million-euro ($22.6-million) line of credit to the Russian company “International Credit Bureau,” according to documents obtained by Meduza. Rietumu bank did not respond to Meduza’s questions for this article.

Based on records, MKB’s owners held meetings in a building at 8 Elizabetes Street in Riga. According to Latvia’s commercial registry, Malikov owns a real estate management company called “Elizabetes 8.” Malikov’s partner in this business was former deputy head of Riga’s economic police department Nils Zhuravlev, who was forced to resign after a corruption scandal involving his acquisition of valuable real estate and automobiles while working as a public servant. After stepping down, Zhuravlev managed Latvia’s Boxing Federation and ran several times in regional elections. Sergey Malikov also showed an interest in politics: in particular, he financed the Social Democratic Party “Harmony,” which is led by former Riga Mayor Nils Usakovs. Malikov did not find time to speak to Meduza.

Back to Russia

The International Credit Bureau has a great deal in common with another credit organization: the Moscow Mortgage Company (MZK), which operates according to similar principles. In the fall of 2016, videos appeared on YouTube, recorded at some kind of staff meeting, discussing how to explain to clients the need to sign over their apartments as loan collateral, and how clients should be given incomplete copies of their loan agreements. The name of the business isn’t mentioned in the video, but the Moscow Mortgage Company later got a court to have the footage blocked in Russia. The identity of the staff member leading the seminar isn’t clear in the video, but several MZK clients told Meduza that they believe it’s Nikolai Chigarev, the company’s deputy general director.

In 2015, both MKB and MZK started appearing frequently in news reports, as the number of cheated clients grew large enough to cause a public scandal. The two businesses filed defamation lawsuits (even against state news pundit Vladimir Soloviev), losing case after case. In November 2015, MZK’s ownership was transferred to the offshore company “Lordena Ventures,” which was registered in the British Virgin Islands.

This organization appears in OCCRP’s famous “Panama Papers” investigation, which was based on documents leaked from the Panamanian law firm and corporate service provider “Mossack Fonseca.” According to those documents, Lordena Ventures had an office in Latvia, located in the Rietumu bank building in Riga. Oksana Utenkova, an employee at the bank, was listed as the company’s representative.

Journalists discovered that Utenkova was listed as the representative of more than 500 offshore companies, the offices of which were all registered at the same building. One of these companies, moreover, is implicated in corrupt practices between the Swedish division of the engineering corporation Bombardier and state officials in Azerbaijan. Following OCCRP’s reporting, Rietumu blocked the accounts belonging to the suspicious companies and announced that Oksana Utenkova no longer works at the bank.

According to data from Russia’s Unified State Register of Legal Entities, Lordena Ventures relinquished its shares in MZK, two days after the publication of the Panama Papers. Today, MZK’s main owner is listed as Konstantin Ilyin (through the “November Holdings LLC”). A company by the same name (owned by Ilyin’s son, Alexander) is registered at the same address as the LLC.

Beginning in 2016, Alexander Ilyin worked as a deputy director at the investment firm “VEB Capital,” which belongs to the state-owned development bank “Vnesheconombank.” One of VEB’s projects was the restructuring of “Globex” bank, its subsidiary investment firm “Globex Capital,” and several other programs. As VEB’s representative, Ilyin was on the board of directors at the “Slava” Watch Factory (a development project on Leningradsky Avenue in Moscow) and the “Ural Broiler” poultry farm in Orenburg. In May 2015, Vnesheconombank executives decided to sell half of Globex Capital to November Holdings, which at the time was owned by Nikolai Chigarev, MZK’s deputy general director. A few months later, Alexander Ilyin bought the company.

“Alexander Ilyin was fired in the summer of 2018. VEB.rf has no connection to the business of issuing microcredit loans to individuals,” a spokesperson for VEB.ru (Vnesheconombank’s new name) told Meduza.

At the time of this writing, the last time Globex Capital appeared in the news was when the company reportedly planned to buy the “Rostelecom” office building at Zubov Square in Moscow (the deal ultimately fell through). In the summer of 2018, the company announced a job vacancy for an attorney. The job description laid out the following duties: “Represent the company’s interests in cases involving debt collection under loan agreements (mortgage lending), property rights disputes, and appealing against the actions of state officials, including court marshals.”

In November 2017, MZK CEO Igor Alekseev, MKB deputy general director Roman Guselnikov (who allegedly appeared in the “instructions” video shared on YouTube), and “Best Bank” LLC president Ilya Krasnevsky were arrested on suspicion of fraud. Ninety-nine percent of Krasnevsky’s firm belonged to a Cyprus offshore company called “Westbanq Limited,” which is now owned by the Russian firm MKB and the Latvian company West Kredit. After Latvia’s de-offshorization campaign in 2018, Sergey Malikov acknowledged that he is the sole beneficiary of Westbanq Limited.

One of the people cheated by Guselnikov, Alekseev, and Krasnevsky was a woman named Elena Kulneva. She borrowed money from MZK, signing an acquisition agreement on her apartment and its subsequent lease with Sergey Malikov. Kulneva lost a civil suit to invalidate the contract, but she was recognized as a victim in the felony fraud case. Another victim was a man who received a loan, despite suffering from schizophrenia. He signed over a deed of gift on his apartment to Guselnikov. This is the same individual whose contract was ultimately nullified by a judge. (Meduza knows the identity of this person.)

In March 2019, Moscow’s Tverskoy District Court jailed another four people working at two microfinance institutions (“Moscow Group” and “Parnas”) that issued home equity loans: Oleg Chernega, Andrey Shkarlet, Yulia Lysak, and Olesya Sukhareva. Stanislav Serebyakov, an officer in the Federal Investigative Committee’s Central Investigation Department, is leading two criminal cases against these individuals.

Like Guselnikov, Olesya Sukhareva was involved in contracts tied to MKB and MZK. At her arraignment, Sukhareva maintained her innocence, stating that she was only “a witness to the transfer of money.” In the argot of the microfinance industry, these people acted as “brokers,” seeking out customers and guiding them until a deal was reached.

One method Guselnikov used to attract business was the company “Your Broker,” which he and a woman named Lyudmila Timshova co-founded. In 2017, following criminal charges against Guselnikov, he withdrew from the company’s founders and “Your Broker” rebranded itself as “Pravoaktiv,” now offering “bank and MFO debt relief” services. According to Russia’s Unified State Register of Legal Entities, Lyudmila Timshova’s brother, Yaroslav, owns the company “WinFin,” and he previously owned another credit broker called “United Credit Service.” In some cases, Guselnikov also performed the role of a “holder,” registering “problematic” apartments under his own name, before preparing to sell them.

The home equity loan company “Realty Capital Mortgage Center” is also registered at the Moscow Mortgage Company’s office address. “Realty Capital” belongs to a realtor named Maxim Lazykin, who has participated in a number of deals tied to MKB.

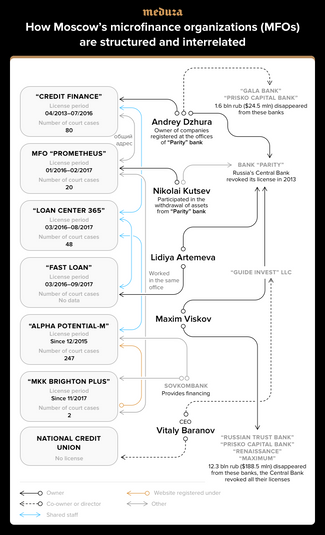

How these microcredit organizations are interrelated

The average lifespan of a microfinance institution that issues home equity loans is about 18 months. Buying a turnkey microfinance company, already registered with Russia’s Central Bank, costs anywhere between 140,000 to 250,000 rubles ($2,160 to $3,850), depending on the enterprise’s history. On specialized Internet forums, you’ll find numerous listings for ready-made MFOs. These companies change their names, while maintaining the same staff, “holders,” and private investors, whose financing is used to attract debtors.

The company “Loan Center 365,” where Natalia Smelnitskaya borrowed money, was created in February 2016 by Anna Sukhanova. According to the Spark-Interfax database, Sukhanova has founded 21 microfinance companies. Meduza found for-sale listings for several of these firms online. A few months after Loan Center 365’s creation, the firm was transferred to Anton Velichko and Latvian national Yulia Kalinina.

Smelnitskaya was one of Loan Center 365’s first customers, signing “contract number four.” According to Meduza’s findings, the company entered into at least another 67 loan agreements between the summer of 2016 and February 2018. Reviewing the records filed with Rosreestr regarding the property owned by the company’s clients, Meduza discovered that 25 of 37 debtors sold their property soon after receiving their loans. In 15 cases, the homes were sold directly to Loan Center 365. Another six homes were sold to Anton Titov (an employee at the firm), “M2-Leasing” CEO Anatoly Fundobny, and Vladislav Snopok (the son of the president of the insurance company “Capital Life”), with each man acquiring two apartments. According to the Moscow City Court’s files, Vladislav Snopok bought at least two more homes that previously belonged to debtors from another microfinance company called “CreditFinance.” Snopok did not respond to Meduza’s questions.

In the paperwork Loan Center 365 filed with Rosreestr to transfer ownership of Smelnitskaya’s apartment, the company accidentally included documents for another apartment that belongs to a debtor from a different microfinance lender called “Fast Loan.” This company is headed by a 25-year-old Belarusian national named Alina Pikulik, who previously served as the “holder” of at least one apartment that used to belong to people who borrowed from CreditFinance.

Besides luring in customers, Loan Center 365 also recruited investors. The company’s now-disabled website offered potential investors the following enticements: 18 percent annual interest rates on home equity loans issued to clients. Documents obtained by Meduza show that individuals like Kirill Ryazanov (the son of former Gazprom deputy chairman Alexander Ryazanov) took advantage of this opportunity. Another investor was Sergey Zhitchenko, a major entrepreneur in Moscow’s Ruzsky District, who owns commercial real estate, and several markets and popular restaurants, as well as the land surrounding the “Annino” landfill site (one of the biggest in the Moscow region). Zhitchenko started acquiring most of his assets in 2014, when Maxim Tarakhanov, an attorney from Tyumen, was head of the Ruzsky District. In early 2019, Tarakhanov took a job at City Hall, where he now supervises Moscow’s district officials.

Loan Center 365’s investors also include Yuri Dyachkov, the retail business development director for the bank “Finservice.” He, too, has ties to Moscow’s Ruzsky District. In 2017, Dyachkov and Ruzsky District officials created a foundation to support the Holy Mother Cathedral in the town of Novovolkovo, located about 70 miles west of Moscow. Additionally, Dyachkov has his own microcredit business: the company “North-West Partnership,” which issues loans through a website. Kirill Ryazanov, Sergey Zhitchenko, and Yuri Dyachkov all refused to speak to Meduza for this article.

A law against the “evictors”

In early May 2019, a job posting appeared on the website HeadHunter for the position of “evictor,” with a starting monthly salary as high as 160,000 rubles ($2,466). The core responsibilities included: “Collecting overdue debts on home equity loans, and organizing the eviction of debtors from mortgaged real estate.” The vacancy was posted by the microfinance company “Brighton Plus,” which calls itself one of the leaders of Russia’s home equity lending market. Brighton Plus says it issues loans worth 100 million rubles ($1.5 million) every month, made possible by “vigorous investor financial support.” According to Russia’s Unified State Register of Legal Entities, the company is owned by four people, most of whom have no business experience.

Brighton Plus’s website is registered under another legal entity: “Alpha Potential-M” LLC, which also issues microloans. That company’s owners include Anatoly Gramakov (the owner of “Medinar,” a network of affordable housing for workers) and two young people with no business experience. At HeadHunter, Alpha Potential-M describes itself as “a leader in home equity loans” and as a “joint project with Sovcombank.” According to the Federal Notarial Chamber’s loan-collateral records, both companies sign over their clients’ mortgaged homes to Sovcombank, which now holds 86 mortgages on apartments that belonged to Brighton Plus debtors, and 272 that belonged to Alpha Potential-M customers. “The companies have no connection to the bank’s beneficiaries, but they are the bank’s clients. Due to bank secrecy, we do not comment on customer relations and operations,” Sovcombank press secretary Darya Piven told Meduza.

Many clients of these two businesses have also lost their homes. There are currently 242 court cases involving Brighton Plus and Alpha Potential-M filed with the Moscow City Court. In these proceedings, Alpha Potential-M has been represented by attorney Georgy Polyakov, who previously worked for Loan Center 365 and CreditFinance.

Experts argue that microfinance institutions have been able to fool debtors out of their homes so often because the industry is under-regulated. “For years, MFOs have enjoyed a comfortable regulatory environment without limits on loan interest rates, which have exceeded 800 percent a year. Existing regulations do not prevent microfinance organizations from using questionable schemes to legalize their income. Several years ago, the owner of one MFO was arrested for cashing out federal subsidies paid to multiple-child families. The requirements imposed by the Central Bank and the control over the activities of more than 2,000 MFOs are far lower than the regulations enforced against [Russia’s] 473 banks,” says Dmitry Yanin, the head of the International Confederation of Consumer Societies.

“Microfinance organizations are subject to the law against the legalization of criminal proceeds, but the Central Bank and the Federal Financial Monitoring Service exert less control over their work than they do over banks,” agrees Rostislav Kokorev, the head of Moscow State University’s Financial Literacy Laboratory.

But the situation seems to be changing. In April 2019, lawmakers in the State Duma introduced draft legislation that would ban microfinance institutions from issuing home equity loans to individuals. Technically, this bill would amend Russia’s existing law against the laundering of illegally obtained income and financing terrorism, and regulations on microfinance activities and microfinance institutions. Judging by the legislation’s coauthors (which include the speakers of both houses of parliament, Vyacheslav Volodin and Valentina Matviyenko), the bill has a good chance of passing.

Story by Ivan Golunov, edited by Alexey Kovalev

Translation by Kevin Rothrock